December closed out 2025 with a noticeable lift in activity, and early 2026 forecasts suggest more transactions ahead.

Existing home sales in December 2025 totaled 345,000 (non-seasonally adjusted), up +16.9% from November and +4.9% year over year, according to the National Association of Realtors (NAR). For the full year, 2025 ended essentially flat at 4,061,000 compared to 4,062,000 in 2024.

Inventory is still tight. At the end of December, 1.18 million homes were on the market, down -18.1% from November, but +3.5% higher than a year ago, according to Zillow. Month to month, supply shrank. Year over year, it improved slightly.

Home prices remain steady overall. NAR reported a +0.4% YoY increase in December to $405,400 nationally. The Midwest and Northeast saw price growth above +3%, while the West declined -1.4%.

The Mortgage Bankers Association (MBA) reported the national median existing home price at $409,200, up +1.2% YoY. The Midwest led at +5.8%. The Northeast (+1.1%), South (+0.8%), and West (-0.9%) were largely unchanged.

Mortgage rates ended 2025 at 6.2%, according to MBA and Fannie Mae. Fannie expects rates to ease to 6.0% by mid-2026 and remain there through 2027. MBA projects the 30-year fixed rate holding between 6.1% and 6.3%.

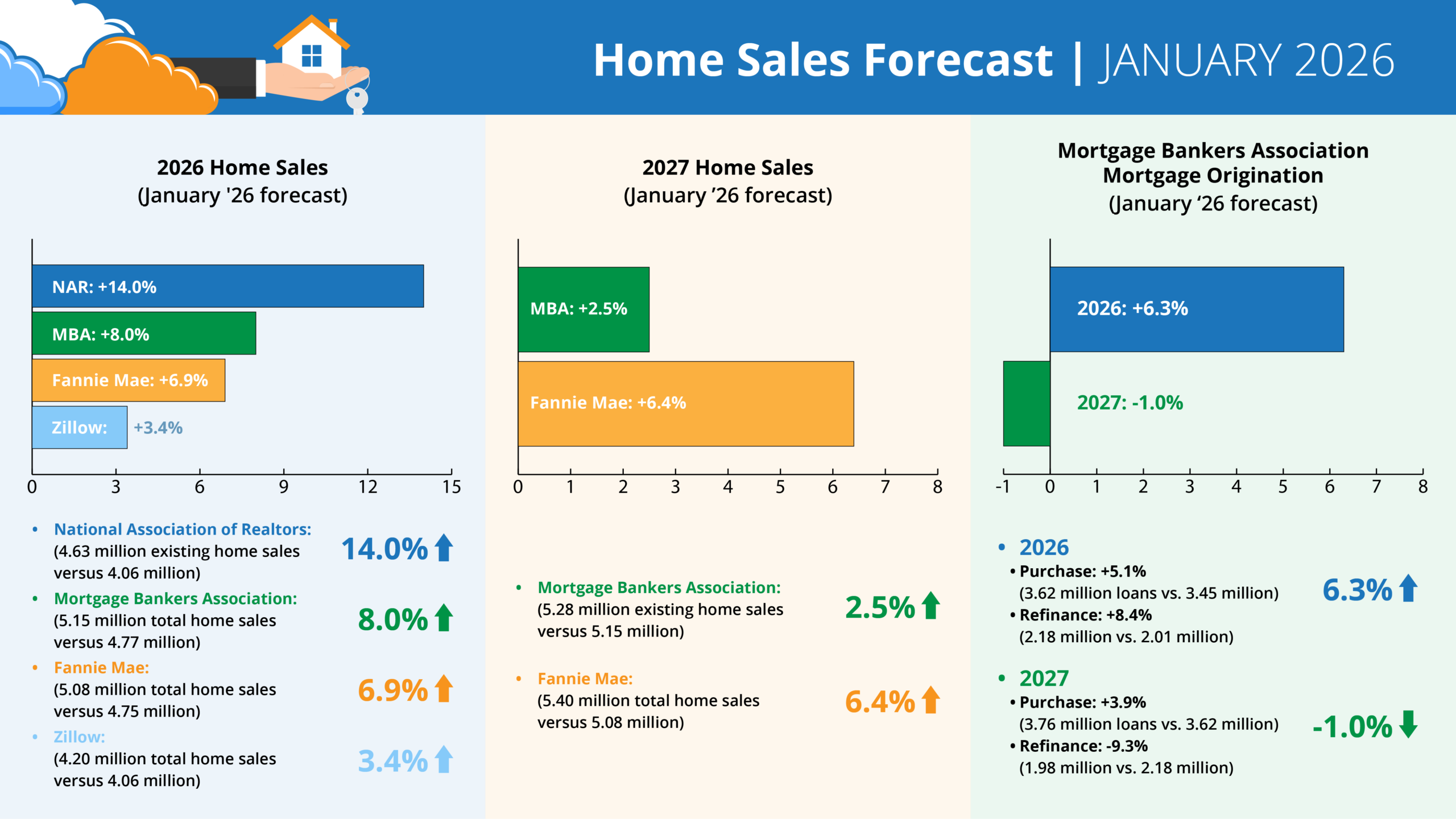

2026 and 2027 sales outlook

January 2026 projections show expected sales growth next year:

- NAR: +14.0% (4.63 million existing home sales vs. 4.06 million)

- MBA: +8.0% (5.15 million total home sales vs. 4.77 million)

- Fannie Mae: +6.9% (5.08 million total home sales vs. 4.75 million)

- Zillow: +3.4% (4.20 million existing home sales vs. 4.06 million)

For 2027:

- MBA: +2.5% (5.28 million vs. 5.15 million)

- Fannie Mae: +6.4% (5.40 million vs. 5.08 million)

Mortgage originations

MBA’s January forecast projects:

2026 total mortgage originations: +6.3% (5.80 million loans vs. 5.46 million)

- Purchase: +5.1% (3.62 million vs. 3.45 million)

- Refi: +8.4% (2.18 million vs. 2.01 million)

2027 total mortgage originations: -1.0% (5.74 million vs. 5.80 million)

- Purchase: +3.9% (3.76 million vs. 3.62 million)

- Refi: -9.3% (1.98 million vs. 2.18 million)

This isn’t a surge. It’s a slow climb. If volume rises in 2026, how quickly you inspect and deliver reports will matter.